A Dummy's Guide To Investing Wisely

Investing 101: Because Ramen Noodles Can’t Be Your Retirement Plan

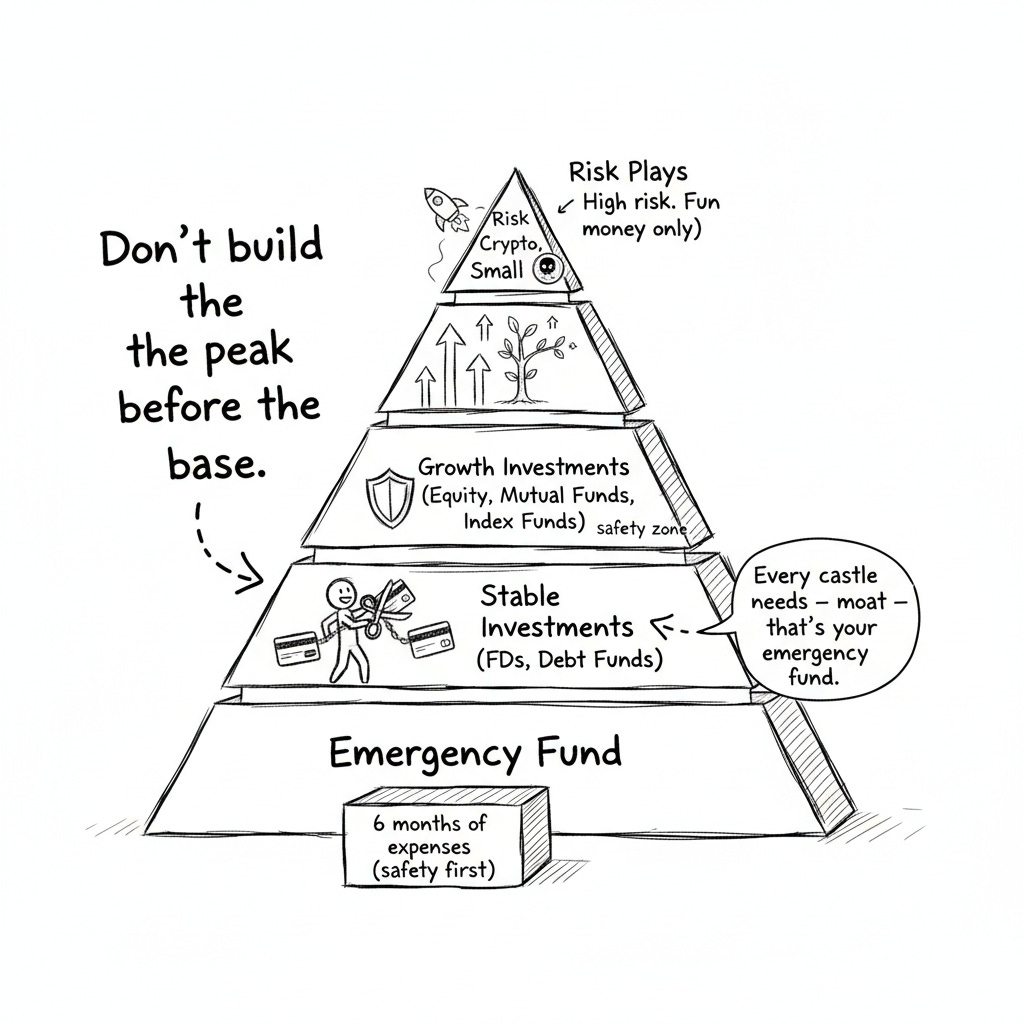

Before I even think about investing, I need to get some basics straight. Seriously. I can’t romanticize the idea of “making money grow” without addressing what needs to be in place first. You can’t build a house without a foundation, and my finances are no different. So, let’s talk.

Return Rates Depending on Investment Choice

Every investment carries its own expected returns, and the risk varies accordingly. Here’s what I’m looking at:

Savings Bank Account? Forget it. Around 2.5%. It’s more like keeping money under a mattress.

Liquid Debt Mutual Funds? Decent. 7%. Almost like an FD but with better liquidity.

Gold? Solid. 9%. Good hedge against inflation.

Index Funds? Reliable. 15%. Ride the economy’s growth wave.

Real Estate? Wild card. 12-20% but very market-dependent.

Small Cap Mutual Funds? Big potential, bigger risk. 18-25%.

Government Bonds? 6-8%. Safe but modest.

These numbers aren’t set in stone, though. For instance, as of 2023, the Indian equity market has seen a resurgence post-pandemic, with Nifty 50 delivering around 18% CAGR over the last five years. Meanwhile, the US market, particularly the S&P 500, has been volatile due to inflation concerns and Fed rate hikes, but still offers long-term stability.

Emergency Fund

This is non-negotiable. Imagine my car breaking down, a medical emergency, or, God forbid, losing my job. I need a cushion.

The rule is simple: 6 months of expenses. If I spend ₹30,000 monthly, I need ₹180,000 saved up.

How? Split it up:

25% in my savings account. Immediate access.

75% in a liquid debt fund. Slightly better returns and still accessible.

Don’t touch investments until this fund is ready. Seriously. I’ll thank myself later.

Choosing Mutual Funds

It’s not just about picking a fund that sounds cool or has a shiny brochure.

Always go for Direct Plans. Lower fees. Better returns.

Look at metrics like:

Alpha: How much extra this fund earns compared to the market. Bigger is better.

Beta: Volatility. Lower means less risk.

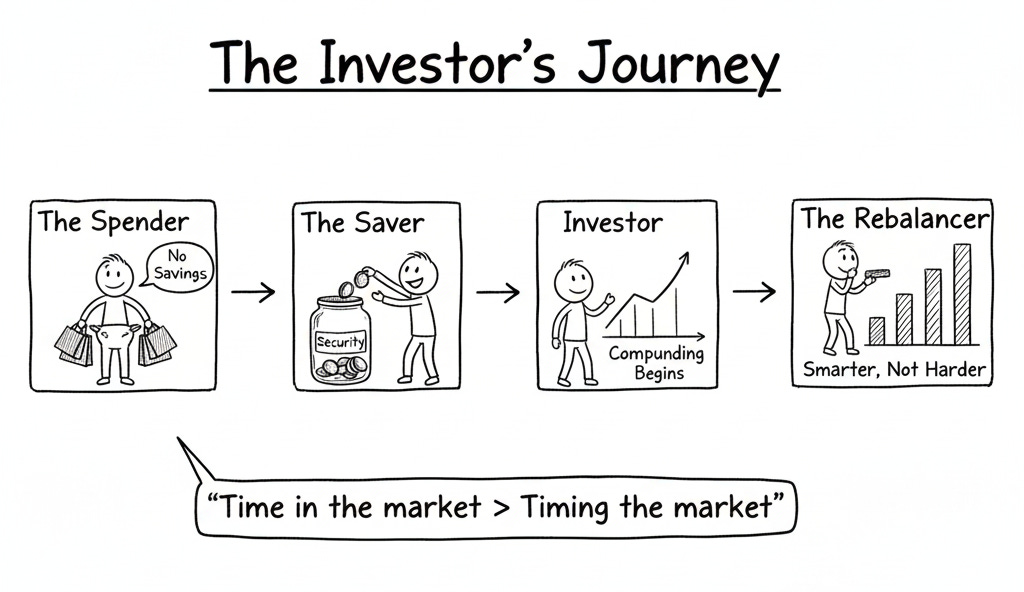

Long-term only. 3-5 years minimum. This isn’t a quick money scheme. Let compounding do its thing.

For example, as of 2023, Indian mutual funds like Axis Bluechip Fund have delivered a 5-year CAGR of around 18%, while US-based funds like Vanguard’s S&P 500 ETF have averaged 10-12% over the same period.

Building a Good Investment Basket

Let’s assume I’ve got ₹100,000 to save every month. Spread it around:

20% Gold. Solid foundation.

20% Foreign Stocks. Exposure to the US markets or others (JP, KOR, SINGAPORE).

30% Large Cap Funds. Stability with decent growth.

20% Mid Cap Funds. Balanced risk and return.

10% in risky plays—Smallcaps, Bitcoin, Meme Coins, whatever. Fun, but don’t bet the farm.

Minimize Overlap. Don’t invest in 10 funds that all target the same sectors. What’s the point of diversifying if I don’t actually diversify? And go global. If the domestic market takes a hit, international exposure saves me.

Key Metrics I Need to Know

These are my tools. Learn them. Use them.

CAGR: Shows annual growth over time. Example? ₹10,000 grows to ₹20,000 in 5 years. CAGR? 14.87%.

XIRR: Perfect for SIPs or uneven investments. Tracks real annualized returns.

Sharpe Ratio: How much return I’m getting for the risk I’m taking. A ratio of 1.33 means the returns outweigh the risks.

P/E Ratio: How expensive a stock is. A ₹500 stock with ₹50 EPS? P/E is 10.

Alpha: Performance beyond benchmarks. A fund returning 15% vs. an expected 12% has an Alpha of 3.

Combine these metrics. None are perfect on their own, but together? They tell a story.

Market Collapses and How to Survive

Market collapses are inevitable. Nassim Taleb’s The Black Swan taught me that rare, unpredictable events can upend even the most stable systems. The 2008 financial crisis, the 2020 pandemic crash—these are reminders that markets are fragile.

So, how do I survive?

Goal-Driven Investing: Define clear goals. Retirement? A house? A vacation? Goals dictate strategy. If I’m investing for a 20-year horizon, short-term crashes shouldn’t faze me.

Diversification: Don’t put all eggs in one basket. Spread across asset classes, geographies, and sectors.

Emergency Fund: Already covered this, but it’s worth repeating. A cushion ensures I don’t liquidate investments at a loss during a downturn.

SIPs: Systematic Investment Plans average out market volatility. When markets are down, I buy more units at lower prices.

Avoid Panic Selling: Emotional decisions are the enemy. Stick to the plan.

For example, during the 2020 crash, the S&P 500 dropped 34% in a month but recovered fully within six months. Those who held on or invested during the dip reaped significant rewards.

Additional Tips

Rebalance Regularly: Market changes? Adjust accordingly. If one asset class outperforms, it might skew my portfolio. Rebalancing brings it back in line.

SIPs Are My Friend: They average out market volatility.

Understand Debt: Home loans? Good. Credit card debt? Bad.

Invest in Myself: The best investment I can make is in my skills and knowledge. Warren Buffett wasn’t wrong.

Quotes to Remember

Time in market > Timing the market.

A budget is telling your money where to go instead of wondering where it went.

Do not save what’s left after spending; spend what’s left after saving. — Warren Buffett

The stock market is a device for transferring money from the impatient to the patient. — Warren Buffett

The best investment you can make is in yourself. — Warren Buffett

Investing isn’t glamorous. It’s not fast or thrilling. It’s deliberate. Methodical. And the best part? It works.

References and Further Reading

The Black Swan by Nassim Taleb

The Intelligent Investor by Benjamin Graham

Common Stocks and Uncommon Profits by Philip Fisher

A Random Walk Down Wall Street by Burton Malkiel

These books have shaped my understanding of markets, risk, and the importance of patience. They’re worth revisiting whenever I feel lost in the noise of daily market movements.

This removes the mystique without dumbing it down. The order of operations is the real lesson.

Here's the TL;DR version of this:

• Investing fails without a foundation.

• Emergency funds precede market exposure.

• Diversification reduces catastrophic risk.

• Metrics matter more than hype.

• Time compounds faster than tactics.